News: Markets

24 January 2020

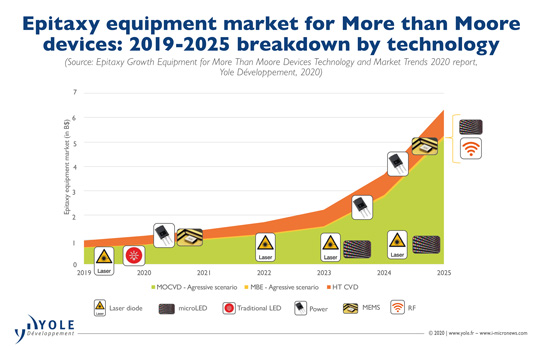

Epitaxy equipment market to grow from $940m to over $6bn by 2025, driven by VCSEL and disruptive LED devices

The epitaxy growth equipment market for ‘More than Moore’ devices was worth nearly $940m in 2019, and is expected to exceed $6bn by 2025 (in an aggressive scenario), according to Yole Développement’s technology & market report ‘Epitaxy Growth Equipment for More Than Moore Devices’.

From a technical point of view, metal-organic chemical vapor deposition (MOCVD) serves most of the III-V compound semiconductor epitaxy industry, such as gallium arsenide (GaAs)- and gallium nitride (GaN)-based devices. High-temperature (HT) chemical vapor deposition (CVD) serves the majority of mainstream silicon-based components and silicon carbide (SiC) devices.

The semiconductor industry has been traditionally dominated by silicon substrates. Although silicon is still by far the most dominant material (with more than 80% market share), alternative non-silicon-based substrates like GaAs, GaN, SiC and InP (indium phosphide) are gaining momentum within the ‘More than Moore’ industry. Indeed, new applications are emerging along with stringent requirements where silicon solutions are not able to provide the performance expected. Innovative substrate materials are hence being considered by semiconductor manufacturers.

GaN material represents the main epitaxy market after silicon substrates, driven mostly by traditional GaN-based light-emitting diode (LED) devices. However, the overall visible LED industry is currently diversifying towards more specialized ultraviolet (UV) and infrared (IR) LEDs based on GaAs substrates. Additionally, manufacturers are developing new types of LEDs to continue creating value in consumer displays, such as mini-LEDs and micro-LEDs. Apple is initiating this with adoption in its higher-end 2021 smartwatch model. In the best-case scenario, micro-LEDs could also spread into smartphone products, which will definitely reshape the epi-ready wafer market, says Yole.

On the other hand, wide-bandgap (WBG) materials like SiC substrates have found opportunities in the power electronics market. Here, power consumption reduction is required for electrification of transportation, renewable energy, motor drives and some power supply applications. Despite the high price of SiC, such substrates represent a strong asset for high-voltage applications, and are thus considered to be a technology choice for some metal-oxide-semiconductor field-effect transistor (MOSFET) and diode products.

Looking ahead, photonics products like vertical-cavity surface-emitting lasers (VCSELs) operating in the IR spectrum (typically processed on GaAs) are making serious inroads into the epitaxy market. In addition, GaAs is especially advantageous for radio-frequency (RF) products such as small-cell implementation, for both sub-6GHz frequencies and the first millimetre-wave (mmWave) small cells in the 28-39GHz range. With the cellphone transition from 4G to 5G, Yole hence expects GaAs to remain the mainstream technology for sub-6GHz frequencies instead of complementary metal-oxide-semiconductor (CMOS) silicon, since it is the only technology able to meet increasing power level and linearity requirements imposed by antenna board-space reductions as well as carrier aggregation and multiple-input multiple-output (MIMO) technology.

Choosing the appropriate substrate technology will depend strongly on the technical performance associated with device requirements, as well as the cost, notes Yole.

“As of today, the epitaxy growth equipment market is mainly driven by LED and power applications,” says Amandine Pizzagalli, technology & market analyst, Semiconductor Manufacturing, at Yole. “In fact, massive subsidies in China have led to an excessive LED capacity build-up. The MOCVD market is now in a situation of significant overcapacity for GaN LED production compared to what is actually produced,” he adds. “MOCVD investment is particularly tough to forecast in the next few years and could change year to year. The situation could be reversed if the government decides to strictly prevent the major LED manufacturers from producing more GaN wafers.”

The report has therefore considered different scenarios for the traditional LED and micro-LED markets.

For traditional GaN-based LEDs, MOCVD investment trends will not follow LED wafer demand. Specific upsides and downsides with respect to GaN LEDs might arise, as used to happen in the past.

Nevertheless, given recent competitive trends in China, the general lighting and backlighting markets have become commoditized. Hence, epitaxy vendors do not expect significant revenue from these markets going forward.

However, requirements for micro-LED epitaxy in terms of defects and homogeneity are more stringent than for traditional LEDs. There are credible roadmaps for improvement in tools and equipment to reach approximately 0.1 defects/cm2 or less, based on defects larger than 1µm. Tighter operating conditions are needed in cleanrooms, including for automation and wafer cleaning, compared with traditional LED manufacturing. This is especially true for the smallest dies (below <10µm), which will have smaller killer defects.

Meanwhile, laser diodes represent an additional fast-growing opportunity as the consumer goods industry massively adopts edge-emitting lasers and VCSELs.

Yole notes that, for compound semiconductor-based devices such as laser diodes, micro-LEDs and VCSELs, the MOCVD reactor market could be affected by possible technology transitions to molecular beam epitaxy (MBE). In fact, MBE could bring greater advantages in terms of yield and uniformity for VCSELs as well as for high-frequency 5G RF applications. In the case of SiC power devices, MOCVD manufacturers are trying to identify and develop new MOCVD technologies to address the SiC market, where HT CVD is currently predominant.